Automotive Joint-Venture Markets in China, How Long Can They Last?

When China first opened their international borders to Western industries in the 1980s, automotive OEM’s were salivating at the potential it offered. Bound to be an economic powerhouse and home to a massive consumer base, who were increasing in affluence, China flashed capabilities that rivaled the United States at that time.

I witnessed this first hand growing up in Shanghai in 1994, as farmlands were transformed into skyscrapers and super highways (almost overnight), and the city instantaneously became a metropolis. At the time, foreign automotive companies possessed nearly 100% of the market share, particularly German and American manufacturers, who jumped on the opportunity to enter the market first.

What goes up, must come down.

In order to gain market access, the Chinese government required that automotive OEM’s partner with a local firm in order to exchange knowledge, technologies and begin developing domestic branded automobiles. However, a lot has changed since then, and in 2015 multinationals are experiencing stricter joint-venture regulations and intense competition. The result being that China is not as profitable as it once was. With a market that is beginning to show signs of vulnerability, at what point will multinationals shift their focus from China to India, South East Asia or even Africa?

So, what exactly changed over these 30 years?

Let’s start with the basics, primarily the rise in production costs.

The average wage in China has risen exponentially due to improved living standards, and this is no exception to the factory employees. In fact, factory jobs have taken one of the biggest hits, due to the fact that the pay is low compared to other lines of work, and the majority of young citizens are pursuing university degrees to avoid exactly this type of employment. Although most car production sites have switched to autonomous or robotic production, factory workers still consist of hundreds if not thousands of employees at each production site, making it tough for OEM’s to find suitable employees with low wages.

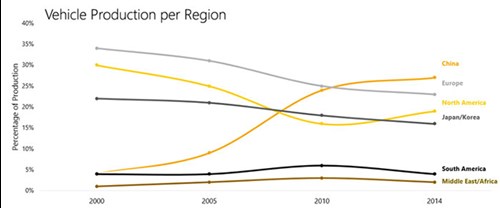

Source: ACEA, The Automobile Industry Pocket Guide, 2015

Also of high importance are the joint-venture agreements, which have been regularly getting stricter.

Previously, the common approach had been that the foreign OEM maintained at least a 51:49 parity if not more, in order to control both the strategy and direction of the joint-venture. Recently, the trend has shifted to favor the local partners, including some holding a 50:50 parity. This has caused a clash of interest as foreign and domestic OEM’s often have differing long-term interests and strategies. The stricter government pressure to invest in developing regions, such as in Volkswagen’s case to invest a 3 billion dollar production site in rural Xin Jiang, is also becoming an obstacle for multinational corporations.

Is there such a thing as too much competition?

Another shift in the market has been increasing competition both locally and internationally.

Local producers like Chang An, Dong Feng, Geely, Great Wall, BYD and others have begun to make a name for themselves in the Chinese market. While their brands cannot be compared to automobile giants like Toyota, Volkswagen or Ford, they have been steadily gaining market share to 22%. However, the market share is closer to 50% when including all motor vehicles from trucks to buses to two/three wheelers. On top of this, foreign automobiles have to endure an import tax, consumer tax and value-added tax, causing their vehicles to be 1.5 to 2.5 times more expensive than in the West. This ensures that only the upper middle class and upper class citizens can afford them, while the working class which comprises the majority of the roughly 1.4 billion person nation, tend to target the local brands.

Finally, the growth ratio of the automobile market has begun to show signs of regression, with a current growth ratio of roughly 7.4% (KPMG, 2014).

The market has begun to saturate, as the young generation slowly loses interest in owning a vehicle, and the second hand car market grows at an alarming rate. In fact, a large portion of the vehicles produced in China today, are not sold in China but instead in neighboring countries. At the same time, India and South East Asia are growing at a double digit growth ratio alongside other trends such as urbanization and increase in standard of living. Because of this, multinationals such as Toyota have begun developing production centers in Thailand, while Ford has begun to focus on production in Mexico so a trend is clearly unfolding.

This is not to say that it is all bad news in China.

In fact, chances are that the automobile market in the People’s Republic will remain the largest globally by a significant margin for decades to come. China is still solely responsible for 25-30% (KPMG, 2014) of all vehicles sold globally and the production numbers are not far off at 27% (ACEA, 2015). Additionally, while the growth has slowed down even amongst foreign OEM’s, most of the big players are still experiencing growth ratios that would be considered significant in the Western hemisphere. For example, as of Q1 2015, BMW experienced a growth of 5.4%, compared to Audi at 6.1% and Mercedes at 15.0% (Forbes, 2015).

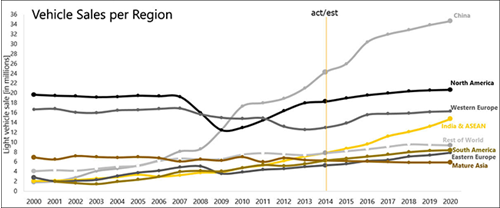

Source: KPMG, Executive Survey, 2014

Chinese consumers valued purchasing a car as much as purchasing a house.

Another benefit to China is the differing culture when compared to Westernized countries, particularly when it comes to affluence and status. In China, significant number of citizens have recently reached the middle class or upper class and one of their priorities remains to purchase a vehicle as soon as possible. In fact, a study (McKinsey, 2012) found that Chinese consumers valued purchasing a car as much as purchasing a house and providing for their children’s education. Particularly, they target foreign branded automobiles as they display a sign of fortune, wealth and a certain lifestyle. On top of this, the extremely wealthy citizens in China, are known to purchase multiple luxury vehicles as collectibles. You would be surprised at how many times I have walked into a parking garage and seen a line of Ferraris, Lamborghinis and Porsches owned by just one person or family.

Finally, the risk averse producers will still remain in China, as it is a proven economy that has been beneficial for OEM’s for over 25 years. The fact is that regions like South East Asia, India or Africa might be enticing but come with a level of risk and there is no guarantee they will experience similar success as China, at least not in the next decade. Some producers may simply decide to play it safe and remain in an economy that still offers positive growth and profits.

So what do you think will happen? Which country has the potential to be the next China?

China has been and still is the frontrunner in the automobile industry, both in production and sales. It remains an attractive destination for multinational OEM’s but the cracks have begun to show. What will occur in the long-term is anybody’s guess, but what we do know is that growth is slowing, the market is saturating and the regulations as well as competition are heating up. Multinationals are taking notes of this, weighing their options and already planning their next market to enter.